Futures Market: Last Friday night, LME copper opened at $9,536.5/mt, fluctuated considerably from the beginning to the middle of the session, peaked at $9,567.5/mt near the end, then dropped back slightly to a low of $9,497/mt, and finally closed at $9,515.5/mt, down 0.44%. Trading volume reached 18,900 lots, and open interest stood at 292,000 lots. Last Friday night, the most-traded SHFE copper 2504 contract opened at 77,350 yuan/mt, quickly peaked at 77,700 yuan/mt, fluctuated downward to a low of 77,400 yuan/mt during the session, then rebounded to form a "V-shape," peaked at 77,680 yuan/mt near the end, and finally pulled back slightly to close at 77,630 yuan/mt, up 0.12%. Trading volume reached 20,000 lots, and open interest stood at 172,000 lots.

[SMM Copper Morning Meeting Notes]

News: (1) According to the latest monthly report by the International Copper Study Group (ICSG), the global refined copper market recorded a supply deficit of 22,000 mt in December 2024, compared to a deficit of 24,000 mt in November. ICSG stated that the market is expected to see a surplus of 301,000 mt in 2024, following a deficit of 52,000 mt in the previous year. In December, global refined copper production was 2.37 million mt, while consumption was 2.39 million mt.

Spot Market:

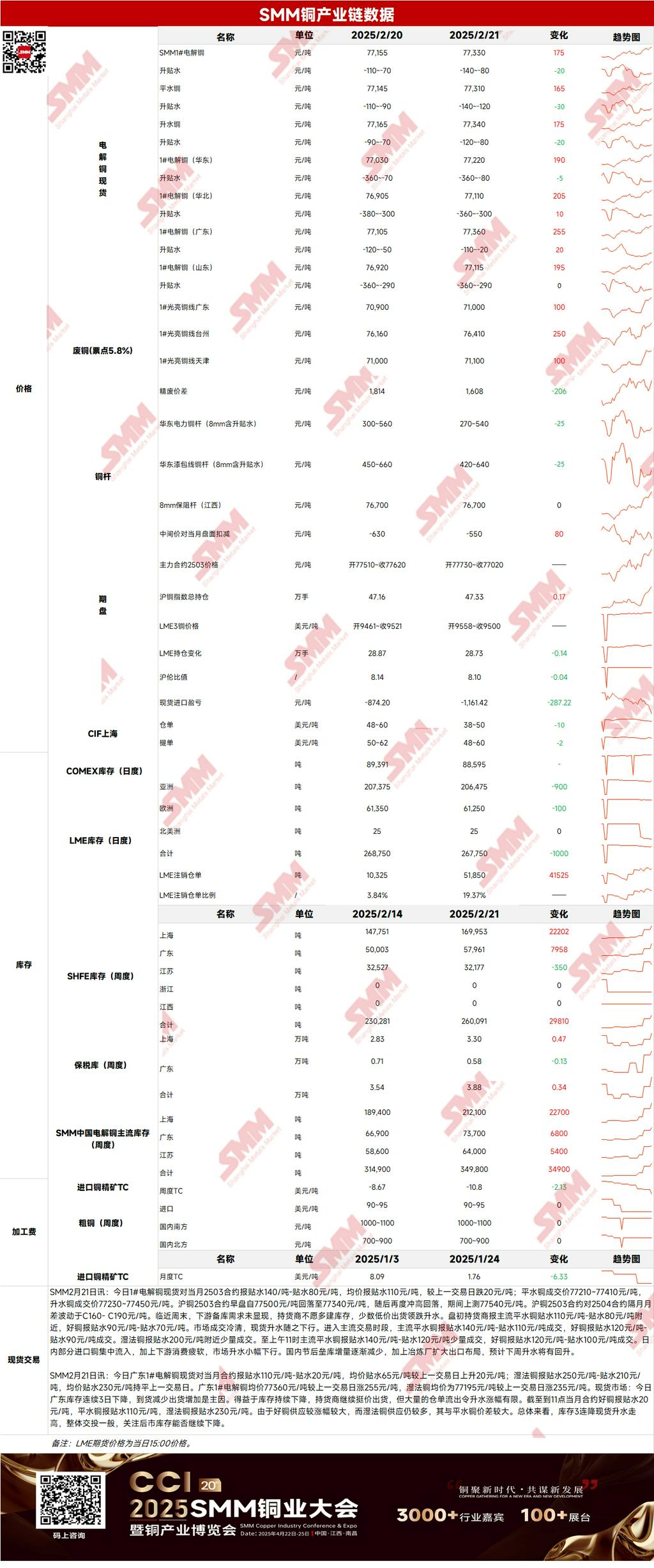

(1) Shanghai: On February 21, mainstream standard-quality copper was quoted at a discount of 140-120 yuan/mt against the front-month contract, while high-quality copper was quoted at a discount of 120-80 yuan/mt. During the day, some imported copper flowed into the market, and weak downstream consumption led to a slight decline in premiums. The post-holiday inventory buildup in China has gradually slowed, and smelters have expanded their export layouts. Premiums are expected to rebound next week.

(2) Guangdong: On February 21, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 110-20 yuan/mt, with an average discount of 65 yuan/mt, up 20 yuan/mt from the previous trading day. Hydro copper was quoted at a discount of 250-210 yuan/mt, with an average discount of 230 yuan/mt, flat compared to the previous trading day. The average price of #1 copper cathode in Guangdong was 77,360 yuan/mt, up 255 yuan/mt from the previous trading day, while the average price of hydro copper was 77,195 yuan/mt, up 235 yuan/mt from the previous trading day.

(3) Imported Copper: On February 21, warehouse warrant prices were $38-50/mt, QP March, with an average price down $10/mt from the previous trading day. B/L prices were $48-60/mt, QP March, with an average price down $2/mt from the previous trading day. EQ copper (CIF B/L) was quoted at $2-10/mt, QP March, with an average price down $1/mt from the previous trading day. These quotes referenced cargoes arriving in late February and early March. The SHFE/LME price ratio continued to deteriorate, and suppliers sold bonded warehouse warrants at low prices due to concerns over increased exports by domestic smelters. However, tight supply of forward B/Ls kept registered B/Ls and EQ cargoes firm. The premium for warehouse warrants and B/Ls inverted, and buyers and sellers had significant disagreements.

(4) Secondary Copper: On February 21, secondary copper raw material prices rose by 100 yuan/mt MoM. Guangdong bare bright copper prices were 70,900-71,100 yuan/mt, up 100 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 1,608 yuan/mt, down 206 yuan/mt MoM. The price difference between copper cathode and rod made from scrap was 955 yuan/mt. According to an SMM survey, Ningbo import traders reported that the Beilun Port Zhongda Xie Terminal is preparing to construct a container berth, a project expected to last one year. During the construction period, inspection sites and container yards will be affected, causing port congestion at Zhongda Xie Terminal and impacting customs clearance efficiency.

(5) Inventory: On February 21, LME copper cathode inventory decreased by 1,000 mt to 267,750 mt. On the same day, SHFE warrant inventory increased by 21,622 mt to 154,085 mt.

Prices:

Macro side, investors consolidated positions ahead of the weekend, anticipating more inflation data (e.g., PCE) this week and closely monitoring tariff-related headlines. The US dollar strengthened, weighing on LME copper. Additionally, if relations between Trump, Zelensky, and the EU further deteriorate or new tariff policies emerge, the US dollar may continue to rise, further pressuring copper prices. Fundamentals side, copper prices fluctuated, with downstream procurement sentiment remaining moderate and focused on just-in-time procurement. Meanwhile, the export window opened due to tariff impacts, and smelters began planning exports, reducing the amount of tradable copper in the market. This may slow the domestic inventory buildup to some extent. Premiums are expected to rebound this week. In terms of prices, with tariff sentiment fluctuating and domestic policy expectations remaining positive, copper prices are expected to fluctuate at highs today.

[The information provided is for reference only. This article does not constitute direct investment research advice. Clients should make decisions cautiously and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.]